Reimbursement of utility costs is not subject to Law No. 44-FZ

Home → Articles → Reimbursement of utility costs is not subject to Law No. 44-FZ

Which paragraph of the Federal Law dated 04/05/2013 No. 44-FZ “On the contract system in the field of procurement of goods, works, services to meet state and municipal needs” (hereinafter referred to as Law No. 44-FZ) can the customer - a municipal unitary enterprise - be guided by when concluding a contract? to reimburse the costs of consumed electricity, if the contract is concluded with a budgetary institution (kindergarten), the contract price is over 100 thousand rubles?

Reimbursement of expenses for utility bills in relation to premises leased is not specified in the Federal Law of 04/05/2013 No. 44-FZ “On the contract system in the field of procurement of goods, works, services to meet state and municipal needs” (hereinafter referred to as the Law No. 44-FZ) as an independent basis for concluding an agreement with a single counterparty. Nevertheless, representatives of the Ministry of Economic Development of Russia have repeatedly expressed the opinion that an agreement to reimburse the costs of the lessor (lender) for utilities and operating services can be concluded between this person and the tenant (borrower) without conducting competitive procedures, in particular, in accordance with paragraph. 8 hours 1 tbsp. 93 of Law No. 44-FZ, which provides for the opportunity to conclude an agreement with a single counterparty for the provision of services for water supply, sewerage, heat supply, gas supply (except for services for the sale of liquefied gas), for connection (connection) to engineering networks regulated in in accordance with the legislation of the Russian Federation to prices (tariffs), for storage and import (export) of narcotic drugs and psychotropic substances (see, for example, letters of the Ministry of Economic Development of Russia dated October 25, 2016 No. D28i-2921, dated 09.09.2016 No. D28i-2356, dated 09.08. 2016 No. D28i-2470, dated July 15, 2016 No. D28i-2521, dated May 20, 2015 No. D28i-1442, dated April 30, 2014 No. D28i-734). The letter of the Ministry of Economic Development of Russia dated May 20, 2015 No. D28i-1442 indicated the possibility of reimbursement by the tenant of the landlord’s expenses for paying for electrical energy on the basis of clause 29, part 1, art. 93 of Law No. 44-FZ. However, in accordance with this paragraph, the contract can be concluded exclusively with a guaranteeing supplier of electrical energy, which specialists from the Ministry of Economic Development drew attention to in letter No. OG-D28-912 dated January 23, 2017.

At the same time, the approach that assumes the possibility of concluding an agreement to reimburse the landlord for utility bills in accordance with the above-mentioned standards seems to us to be unfounded. The need for the tenant to reimburse the costs of paying for utilities in relation to the premises leased, which are borne by the lessor, follows from clause 2 of Art. 616 of the Civil Code of the Russian Federation, according to which the tenant is obliged to maintain the property in good condition, carry out routine repairs at his own expense and bear the costs of maintaining the property, unless otherwise provided by law or the lease agreement. In other words, the tenant’s obligation to reimburse the landlord for the costs of maintaining the property leased is based directly on the law. The conclusion of an agreement on reimbursement of utility costs in this situation is aimed at creating conditions for the tenant to use the property transferred to him in accordance with its purpose. In this case, the customer does not receive any provision in non-monetary form other than that which is the subject of the lease agreement. The agreement on reimbursement of costs for utility bills essentially only determines the procedure in accordance with which the amount of expenses to be reimbursed by the tenant will be calculated (see also the resolution of the Federal Antimonopoly Service of the Far Eastern District dated July 18, 2008 No. F03-A59/08-1/1985). In this case, neither the tenant nor the lessor supplies the other party with goods, performs work or provides any service.

In this regard, we note that the peculiarity of the agreement on reimbursement of expenses for utilities and communication services is that its subject is not these services themselves (since they are provided to the lessor by other persons on the basis of agreements concluded with them), but namely the procedure for settlements between the person who actually consumed the services (the lessee), and the person who purchased them under contracts for the provision of the relevant services (the lessor). Relations for the provision of services of water supply, sanitation, heat supply, gas supply, energy supply, etc. (subject to the regulation of clauses 8 and 29, part 1, article 93 of Law No. 44-FZ) does not arise between the tenant and the landlord, regardless of whether this is indicated in the lease agreements (see, for example, clause 22 of the Review of Permission Practices disputes related to rent, reported by information letter of the Presidium of the Supreme Arbitration Court of the Russian Federation dated January 11, 2002 No. 66). Therefore, if the landlord’s expenses for paying for utilities are not taken into account in the lease agreement as, for example, a variable component of the rent, then there are no grounds for concluding a separate contract between the tenant and the landlord for the reimbursement of such expenses.

Finally, one cannot fail to take into account that the obligation to reimburse the landlord’s expenses arises from the tenant to a certain person, that is, the customer cannot determine another person in principle. Therefore, we believe that relations associated with reimbursement by an enterprise renting premises in a building of the costs of the lessor (subscriber under relevant agreements with resource supply organizations) for payment of utility bills are not subject to Law No. 44-FZ.

Let us note that our point of view regarding the reimbursement of the landlord's expenses for utility bills is our expert opinion, not directly confirmed by law enforcement practice. However, indirect confirmation of this legal position can be found in judicial practice concerning the application of the Federal Law of July 21, 2005 No. 94-FZ “On placing orders for the supply of goods, performance of work, provision of services for state and municipal needs,” which, in its scope of application, is practically identical to Law No. 44-FZ. When considering such issues, the courts in various situations noted that the provisions of the said federal law are not applicable to relations for reimbursement of expenses based on legal requirements (see, for example, resolutions of the Federal Antimonopoly Service of the Ural District dated August 18, 2011 No. F09-5089/11, Sixth Arbitration Court of Appeal dated October 17, 2013 No. 06AP-4213/13, Fifth Arbitration Court of Appeal dated December 11, 2012 No. 05AP-8441/12). For official clarifications, you can contact the Ministry of Finance and the Federal Antimonopoly Service of Russia (clauses 1, 2 of the Decree of the Government of the Russian Federation dated August 26, 2013 No. 728).

Answer prepared by: Olga Zhguleva, expert of the GARANT Legal Consulting Service Quality control of the response: Alexey Alexandrov, reviewer of the GARANT Legal Consulting Service

Latest news of the digital economy on our Telegram channel

| Have you decided to participate in the auction? Obtain an electronic signature (EDS) for auctions and trading platforms from a reliable certification center. Leave a request >> |

Watch “Housing and communal services: dreams come true” and stay informed

In the online magazine “Housing and Communal Services: Dreams Come True,” our expert Elena Shereshovets explains the complex aspects of legislation in the field of managing apartment buildings and providing utility services. She previously said:

- how can the management authority correctly approve the new amount of payment for residential premises;

- about the nuances of maintaining a register of owners of premises in apartment buildings;

- How can a management company develop tactics for dealing with difficult clients?

- on concluding direct contracts in new buildings;

- about errors in new formulas for calculating heating fees and other topics important for the UO.

Subscribe to the channel and stay up to date with the latest news in the housing and communal services sector!

The debtor reimburses the executor for the costs of limiting or renewing the CG

In a new video, Elena Shereshovets dwelled in detail on the question of how a management organization, homeowners’ association or resource supply organization can correctly record in the accounting department the funds spent on disconnecting and/or connecting the debtor.

If a consumer does not pay for a utility service, then all actions to limit and subsequently resume the service are aimed at making him pay. In this case, the debtor is obliged not to pay the UO/HOA/RSO for these services, but to reimburse them for the corresponding expenses, which corresponds to the wording of paragraphs. 120, 121(1) RF PP No. 354.

That is, these costs are not associated with the provision of the utility service itself. These are the losses of the contractor (part 2 of article 15 of the Civil Code of the Russian Federation). Therefore, the management company/homeowners association or the resource supplier reflects such expenses in accounting as part of other expenses when they are recognized by the debtor (clauses 11, 18 of PBU 10/99).

To explain the situation when and how the debtor for housing and communal services recognizes his obligation to reimburse the expenses of the utility contractor specified in clause 121(1) of the RF PP No. 354, Elena Shereshovets refers to the letter of the Ministry of Finance of Russia dated 02/19/2016 No. 03-03-06/ 1/9336. Find out more about this in the video.

The CG contractor takes into account payment for restriction/renewal services as compensation for losses

When the debtor pays the invoice sent to him, which includes the costs of limiting and (or) resuming the supply of the resource, the executor of the corporate governance must record these incomes as compensation for losses.

According to the Tax Code of the Russian Federation, amounts received as compensation for losses are not subject to VAT. The Resolution of the Presidium of the Supreme Arbitration Court dated September 15, 2009 No. 4762/09 also states that the Tax Code of the Russian Federation does not contain rules allowing to calculate VAT on the amount of losses and demand their recovery taking into account this tax.

If the actions to disconnect, limit and resume public services to the debtor were carried out not by the contractor, but by the contractor, then VAT on the cost of such work is included in the cost of work attributed to expenses taken into account for profit tax purposes (clause 1, part 2, article 170 of the Tax Code RF). You can find out more by looking at the online magazine.

On judicial practice on issues of taxation of income of self-government entities and homeowners' associations

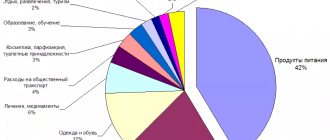

106390

Accounting

The amount of compensation for housing and communal services expenses within the framework of accounting is not recognized as income of the organization. This is explained by the fact that the receipt of these funds into the lessor’s budget does not lead to economic conclusions (clause 2 of PBU 9/99 “Income of the organization”). The landlord is only a transitional link between the tenant and organizations providing utility services.

However, there is an important nuance here. If a company has included reimbursement amounts in income and expenses as part of tax accounting, it is necessary to record a permanent tax liability (PNO), as well as a permanent tax asset (PNA), in accounting. This is confirmed by PBU 18/02 “Accounting for income tax calculations”. PNA and PNO are formed due to constant differences between accounting and tax accounting.

Within the framework of PBU 18/02, permanent differences mean income and expenses taken into account when establishing the income tax base, which are not recognized for accounting purposes as income and expenses of the reporting and next periods (clause 4 of PBU 18/02).

PNO and PNA are recognized by the company in the reporting period in which they are formed. Constant liabilities are equal to the value that is the product of the constant difference of the reporting period and the income tax rate. This refers to the rate established by law and current as of the reporting date (clause 7 of PBU 18/02).

If the company uses PBU 18/02, these postings are applied:

- DT60 KT51. Payment for housing and communal services and communications including VAT.

- DT26 KT60. Accounting for your own expenses for utilities and communication services.

- DT19 KT60. Partial acceptance for VAT offset.

- DT76 KT60. Issuing acts without highlighting VAT.

- DT51 KT76. Receiving payments from tenants.

- DT99 KT68. Permanent tax liability.

- DT68 KT99. Permanent tax assets.

All accounting entries must be based on relevant documents.