Property tax is calculated taking into account the cadastral value of real estate. Depending on the type of real estate (land, private house, apartment, garage, etc.), there are rules for calculating tax based on the cadastral value.

In this article we will briefly and step-by-step analyze examples of calculating tax based on cadastral value in 2021. To do this, we will consider all the components of the tax calculation formula taking into account the types of real estate.

Types of real estate for paying tax at cadastral value

Taxes are imposed only on those properties that are registered in the cadastral register. Registered real estate is assessed by the state and each property has its own cadastral value.

Taxes are paid based on the cadastral value and taking into account tax rates and benefits. Let's look at how taxes are paid based on the cadastral value of the following types of real estate:

- land plot

- residential (private) house

- garden house

- apartment (room)

- other real estate objects

Let us briefly consider the procedure for paying tax at cadastral value in 2021 for each type of real estate separately.

Who has land tax benefits?

In accordance with paragraph 3 of Article 498 of the Tax Code of the Republic of Kazakhstan, the following categories of persons are not recognized as payers of land tax (i.e. are not required to pay it):

- Unified Agricultural Tax payers (farmers, peasant farms);

- government institutions (including correctional institutions);

- religious associations;

- veterans and disabled people of the Great Patriotic War, home front workers, disabled people, orphans under 18 years of age (on land plots with residential buildings, dachas, plots for garages);

- mothers with many children having the title “Mother Heroine”;

- pensioners (if only pensioners are registered at their residence address, without third parties).

Land plot - how to calculate tax in 2021

Land tax is a local tax and is calculated based on the tax rates set by the local municipality. To pay land tax, the following information is required:

- cadastral value of the land plot;

- land area;

- tax rate for a specific land plot adopted by the municipality in 2021;

- availability of benefits for the owner.

When we know all this data, then we can easily calculate the tax on your land plot:

For clarity, here is an example :

| We calculate land tax | Definition, basis, magnitude |

| Taxpayer | Individual – pensioner |

| Land plot | 13 acres |

| Cadastral value | 5 million rub. |

| Tax rate | 0,3 % |

| Federal benefit under Art. 391 item 5 | Reduction of the tax base by 600 sq.m. |

According to the example given in the table, the formula for calculating land tax based on cadastral value is as follows:

(5,000,000 – 2,307,692)*0.3% = 8,077 rub . – the amount to be paid in our case.

(Explanation: if the cadastral value for 13 acres of land = 5 million rubles, then the cadastral value of one hundred square meters = 384,615 rubles, the cadastral value of 6 acres = 2,307,692 rubles - this amount is not taxed; accordingly, only 7 acres are taxed land).

Each specific case will have its own calculation, taking into account the cadastral value, area, rate and benefits. You can read more about the features of calculating land tax here.

Where and how to pay tax?

You can pay tax in different ways:

- at a bank branch using the details;

- in the branches of Kazpost JSC according to the details;

- at the cash desk of the State Revenue Office of the Ministry of Finance of the Republic of Kazakhstan according to the details;

- together with a receipt for payment of utilities (for individuals);

- on the portal Egov.kz;

- through the mobile application of banks (for example, Kaspi.kz);

- through the e-Salyk tax wallet.

Details for paying land tax (as well as penalties and fines) through the cash desks of banks, Kazpost branches or the State Revenue Office of the Ministry of Finance of the Republic of Kazakhstan are as follows:

| Name | Requisites |

| Beneficiary name | Department of State Revenue (for a specific area) |

| Beneficiary BIN | BIN of the territorial State Revenue Office of the Ministry of Finance of the Republic of Kazakhstan |

| Kbe | 11 |

| Beneficiary bank name | State Institution “Treasury Committee of the Ministry of Finance of the Republic of Kazakhstan” |

| IIK | KZ24070105KSN0000000 |

| BIC | KKMFKZ2A |

| KNP | 911 - tax |

| 912 - penalty | |

| 913 - fines | |

| KBK | 104302 - land tax |

BINs of territorial State Revenue Offices of the Ministry of Finance of the Republic of Kazakhstan can be clarified on the website of the tax service as follows.

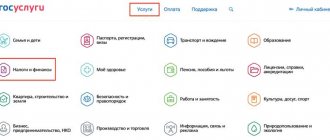

On the Egov.kz portal, tax payment can be made as follows:

- log in to the portal;

- go to the tabs “Home”, “Citizens”, “Customs and taxes”, “Taxation”;

- click on “Order a service online”;

- check the correctness of the IIN (the line will be filled in automatically when logging in to the portal);

- fill in the lines of the form that opens: UGD MF RK, amount, in the line “KNP” indicate “Tax and other obligations”, in the line “KBK” select from the list “Land tax”, “104302”;

- click “Pay” (payment must be made from a card belonging to the person in whose name the land plot is registered).

Within 2 working days, the payment amount will be sent to the budget. The payer will receive an electronic receipt for payment. You can see it in your personal account in the “Service payment history” section.

In order to pay tax through the Kaspi.kz mobile application you need to:

- enter “Payments”, “All”, “Fines and payments to the budget”, “Taxes”;

- then you can select either “Tax on transport, land and property” or “Tax for individuals by details”;

- when selecting “Tax on transport, land and property”, you must fill in the taxpayer’s IIN and click “Check”;

- if there are charges, the tax amount can be paid from the Kaspi Gold card; if there are no charges, the application will issue a notification “No tax charges.”

To pay tax through the e-Salyk tax wallet you need to:

- download the e-Salyk.mobile application and register;

- on “Home” enter “Tax Wallet”, “Tax Calculations”;

- if there are accruals, the amount will be reflected in the subsection “Settlements with the budget”, “Total debt”, broken down by type of tax (CIT);

- opposite each type of accrued tax there is a “Pay” button.

Payment can be made from a linked bank card or from the balance of an electronic tax wallet.

How to calculate residential house tax in 2021

In the same way as the land tax (example above), we can figure out how to pay the tax on a residential building. This is also a local tax, the so-called property tax. Payment of tax on a residential building is regulated by Chapter 32 of the Tax Code.

At the moment, the tax on a residential building is determined based on the cadastral value of the residential building. At the same time, tax payers are exempt from paying for 50 square meters of the total area of this residential building. (Clause 5 of Article 403 of the Tax Code).

For more details on how the tax is calculated based on the cadastral value of a residential private house, read a separate article: “Calculation and determination of the tax on a private residential building based on the cadastral value”

How to check if there is a debt on land tax?

You can check the existence of land tax debt using your IIN:

- by contacting a tax inspector (you must present an identity card);

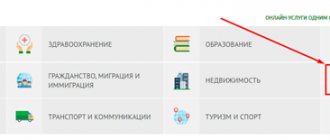

- on the Egov.kz portal: “Home”, “Online services in one list for citizens”, “View and pay tax debts”;

- on the website of the State Revenue Committee of the Ministry of Finance of the Republic of Kazakhstan: “Main”, “Electronic services”, “Business assistance”, “Information on the absence (presence) of debt...”;

- in the bank's mobile application. For example, in the Kaspi.kz application: “Payments”, “Everything”, “Fines and payments to the budget”, “Taxes”, “Tax debts”;

- through the tax wallet (e-Salyk application): “Home”, “Electronic services”, “All services”, “Service for debts on tax and social payments”, enter IIN, “Find”.

Calculating tax on a garden house

There is an opinion that registering your dacha house as a non-residential building is more profitable for paying taxes. But this opinion is wrong. For tax purposes in 2021, a residential building is a house and residential building located on plots for private household plots, individual housing construction, gardening and vegetable gardening.

Therefore, a garden house is also subject to tax, like a residential building, if information about it is included in the Unified State Register of Real Estate. In order to calculate the tax on a garden house, you should also know the components for paying the tax: cadastral value, area, tax rate, availability of tax benefits.

It should be remembered that if your property has several houses - for example, two or three, then tax exemption for 50 sq.m. only applies to one of them.

Who is the payer of land tax? Individuals and legal entities having objects of taxation on the right of ownership, on the right of permanent land use and on the right of primary free temporary land use, except for payers of the unified land tax, religious associations and others.

What is the object of land tax and the tax base? Taxable object - a land plot, with the exception of land plots for public use in settlements, land plots occupied by a network of public state highways, and land plots occupied for objects that are under conservation by decision of the government of the Republic of Kazakhstan, land plots acquired and used for implementation of the investment project. The tax base is the area of the land plot. What are the land tax rates? For tax purposes, depending on the intended purpose, all lands are distributed into categories. At the same time, only agricultural lands, lands of settlements and industrial lands are subject to land tax. The remaining categories of land are taxed only if they are transferred to permanent or primary free temporary land use. Based on this distribution, the basic rates of land tax are established. For example, the basic rates of land tax for agricultural land are set in proportion to quality points per 1 hectare and are differentiated by soil quality from 0.48 tenge to 202.65 tenge. Basic tax rates for agricultural land provided to individuals for personal household (part-time) farming, gardening and dacha construction, including land occupied for buildings, are set in the following amounts: for an area of up to 0.50 hectares inclusive - 20 tenge per 0 .01 hectares; for an area exceeding 0.50 hectares - 100 tenge per 0.01 hectare. Land plots included in the lands of settlements, industry, specially protected natural areas, forest and water resources, used for agricultural purposes, are taxed at the base rates established by Article 378 of this Code, taking into account the conditions of paragraph 1 of Article 387 of this Code. Basic tax rates for land in settlements (with the exception of adjacent land plots) are set per square meter of area depending on the location and name of the settlement, for example in Astana the rate is 19.3 tenge, and in Shymkent - 9.17 tenge, settlements - 0.96 tenge, villages - 0.48 tenge (see Article 381 of the Tax Code of the Republic of Kazakhstan). A residential land plot is considered to be a part of a land plot belonging to the lands of settlements, intended for servicing a residential building and not occupied by the housing stock, including buildings and structures attached to it. Household land plots are subject to taxation at the following basic tax rates: 1) for the cities of Astana, Almaty and cities of regional significance: for an area of up to 1000 square meters inclusive - 0.20 tenge per 1 square meter; for an area exceeding 1000 square meters - 6.00 tenge per 1 square meter. By decision of local representative bodies, tax rates on land plots exceeding 1000 square meters can be reduced from 6.00 to 0.20 tenge per 1 square meter; 2) for other settlements: for an area of up to 5000 square meters inclusive - 0.20 tenge per 1 square meter; for an area exceeding 5000 square meters - 1.00 tenge per 1 square meter. By decision of local representative bodies, tax rates on land plots exceeding 5,000 square meters can be reduced from 1.00 tenge to 0.20 tenge per 1 square meter. Tax rates on land plots occupied for: parking lots, gas stations - lands of settlements are subject to taxation at the base rates for lands of settlements increased by 10 times casinos - lands of settlements occupied by casinos are subject to taxation at base rates for lands of settlements increased 10 times. What is the established tax period? Calendar year What is the procedure for calculating and paying land tax? The tax is calculated by taxpayers (with the exception of legal entities making settlements with the budget in a special tax regime for legal entities producing agricultural products) by applying the appropriate tax rate to the tax base separately for each land plot. Legal entities are required to calculate and pay current land tax payments during the tax period. The amounts of current payments are subject to payment in equal installments no later than February 25, May 25, August 25, November 25 of the current year. The final calculation and payment of land tax is made no later than ten days after the deadline for submitting the declaration for the tax period. When are tax returns filed? The land tax declaration is submitted (with the exception of legal entities carrying out settlements with the budget in a special tax regime for agricultural producers) to the tax authority at the location of the taxable objects no later than March 31 of the year following the reporting year. Calculation of current land tax payments is submitted no later than February 15 of the current tax period. Newly created taxpayers, with the exception of taxpayers created after the deadline for payment of current payments, submit calculations of current payments no later than the 15th day of the month following the month of state registration of the taxpayer. If tax obligations for land tax change during the tax period, the calculation of current payments is submitted no later than February 15, May 15, August 15 and November 15 of the current tax period for taxable objects as of February 1, May 1, August 1 and November 1, respectively Taxation individuals Calculation of land tax payable by individuals is carried out by tax authorities based on the relevant tax rates and tax base no later than August 1. Individuals pay land tax to the budget no later than October 1 of the current year. Source: Tax Code of the Republic of Kazakhstan as of 01/01/2011. Section 14.

How to pay taxes for an apartment and room in 2021

Owners of small-sized apartments will receive good news - apartment living space up to 20 square meters is not subject to tax. m., or rooms - up to 10 sq.m. This benefit is established at the federal level and enshrined in Art. 403 of the Tax Code.

That is, if your apartment is 25 square meters, then in fact only 5 square meters are taxed. There are also additional benefits for paying apartment taxes. These benefits are established at both the federal and local levels. Read our article: “Apartment tax based on cadastral value.”

Tax on other types of real estate at cadastral value

In addition to individuals, legal entities can also be owners of real estate. They are required to pay taxes in advance payments quarterly, and at the end of the tax period submit a tax return. Unlike individuals, organizations are required to independently calculate taxes in accordance with current legislation.

The property tax of organizations is a regional tax and is regulated by Chapter 30 of the Tax Code.

Regarding taxes on personal property. persons, such as outbuildings, garages and unfinished objects - they are also taxed if taken into account by the state.

When is the tax due?

Tax payment deadlines vary for individuals and legal entities:

- individuals make payments once a year, before October 1 of the year following the reporting year (i.e., the tax for 2019 is paid by October 1, 2020);

- legal entities – once a quarter, until 25.02, 25.05., 25.08. and 25.11 of the current year, in equal shares (clause 4 of Article 512 of the Tax Code of the Republic of Kazakhstan).

If you miss the payment deadline, a penalty will be charged for each day of delay (1.25 times the refinancing rate).

Legal entities and individual entrepreneurs are also required to submit current payments to the tax authorities by February 15 of the current year (Article 516 of the Tax Code of the Republic of Kazakhstan). The land tax declaration is submitted until March 31 of the year following the reporting year.

The declaration (form 700.00) reflects not only the land tax, but also the tax on transport and property owned by a legal entity, individual entrepreneur or private practitioner.

The declaration is filled out in accordance with Appendix No. 51 to Order of the Ministry of Finance No. 39 dated January 20, 2020. Forms 700.01-700.03 are attached to it. In particular, information on calculated land tax is contained in Appendix 700.02.