Today, in an accounting educational program, Alexey Ivanov talks about how the Russian system of taxes and fees works, and what specific taxes businesses pay.

Hi all! Alexey Ivanov is with you, the knowledge director of the online accounting “My Business” and the author of the telegram channel “Accounting Translator”. Every Friday on our blog at The Clerk I talk about accounting. I started with the basics, then I will move on to more complex matters. For those who are just preparing to become an accountant, this will help them get to know the profession better. Seasoned chief accountants should look at familiar categories from a different angle.

We continue our tax education. Today we will figure out what taxes there are in our country and where they are paid. Chapter 2 of the Tax Code of the Russian Federation is devoted to this, but I will compress it into one post.

There are three types of taxes and fees in Russia:

- federal;

- regional;

- local.

Federal taxes and fees

In accordance with Art.

12 of the Tax Code of the Russian Federation, federal taxes and fees are such obligatory payments, the transfer of which must be carried out everywhere on the territory of the Russian Federation. At the same time, the effect of federal tax standards is regulated only by the Tax Code of the Russian Federation, which introduces and repeals both the taxes themselves and individual provisions for a particular federal tax. The amounts of federal taxes go to the budget of the same name of the Russian Federation.

The materials in this section will tell you about the procedure for applying the BCC for various taxes..

And the procedure for making an error in the KBK is discussed in detail by ConsultantPlus experts. Get free access to the system and go to the Ready-made solution.

What are the consequences of not paying taxes?

For each day of delay, penalties will be charged. Each day an amount equal to 1/300 of the current refinancing rate of the Central Bank of the Russian Federation of the debt amount will be added to the amount payable.

If you do not pay taxes on time and are very late in payment, sanctions may be applied: freezing of bank accounts, refusal to travel abroad, seizure of property. In some cases, the Federal Tax Service may collect the debt through the court, in which case you will also have to pay an enforcement fee. Finally, owing taxes can negatively impact your credit history, making it difficult to get a loan or mortgage.

Follow the news, subscribe to the newsletter.

When quoting this material, an active link to the source is required.

Regional taxes

Regional taxes, which include transport tax, taxes on gambling and property of organizations, can be regulated both by the Tax Code of the Russian Federation and by laws issued by the authorities of the country's regions, in contrast to federal taxes. The laws of the constituent entities determine the meaning of rates, as well as the availability of certain benefits, specify the terms of payments and submission of declarations.

So, for example, ch. 28 of the Tax Code of the Russian Federation, establishing transport tax rates in paragraph 1 of Art. 361 of the Tax Code of the Russian Federation, in paragraph 2 of Art. 362 of the Tax Code of the Russian Federation indicates that their value can be changed by subjects up or down by 10 times. And the Moscow City Law “On Transport Tax” dated 07/09/2008 No. 33 already sets out the final requirements for calculating the tax, in particular the rates used to calculate the transport tax.

Payment for this type of taxes goes to the budgets of the constituent entities of the Russian Federation.

IMPORTANT! Despite the fact that income tax belongs to the group of federal taxes, payments for it go to 2 budgets: federal and regional (3 and 17%, respectively).

Where and how to pay taxes

Long gone are the days when you had to stand in line at a cash register to pay taxes. Now, for the convenience of taxpayers, there are many services that allow you to pay taxes without leaving your home.

Thus, an individual can pay any of the personal taxes:

- through your bank’s mobile application;

- through online services posted on the Federal Tax Service website: “Taxpayer Personal Account for Individuals”, “Pay Taxes”, application for mobile devices “Taxes for Individuals”.

Through which banks you can pay taxes in the “Taxpayer’s Personal Account for individuals” on the Federal Tax Service website, you can find out in the “ConsultantPlus” system. If you don't have access to K+, get it for free on a trial basis.

Those who prefer to pay taxes the old fashioned way can do this at the cash desk of any bank branch or at any branch of Russian Post.

The last day for paying taxes for 2021 is December 1, 2021 (Clause 1, Article 409 of the Tax Code of the Russian Federation). This date falls on Wednesday - a working day. Consequently, no postponements are provided for this year.

Those who do not fulfill their obligation on time will have to pay a penalty. They will be accrued from the next day, from 12/02/2021. The debt to the state will grow up to and including the date of payment of the debt.

Also, if there is a tax debt, an individual may face a ban on traveling abroad and seizure of bank accounts.

If the tax has to be collected from the debtor by force, the individual will also have to pay the state duty and pay the bailiff (enforcement fee).

Local taxes and fees

The effect of local taxes is regulated by the Tax Code of the Russian Federation and regulations drawn up at the municipal level. These taxes include land tax and personal property tax. And since 2015, a trade tax has been introduced into this group (law dated November 29, 2014 No. 382-FZ).

Read about the procedure and deadlines for paying the trade fee in the materials in the “Trade Fee” section.

Note! From 2021, the deadlines for paying transport and land taxes have become the same, because... regulated at the federal level. They are no longer approved by local and regional authorities. See here for details.

Funds used to pay taxes go to local budgets.

The amount of cadastral value required for calculation

The tax base is determined as the cadastral value of the object as of January 1 of the year, which is the tax period (clause 2 of Article 375 of the Tax Code of the Russian Federation). Therefore, payment of tax is possible only if this value is determined. If not, you will not have an obligation to pay tax due to the lack of a tax base (clause 2 of Article 375, subclause 2 of clause 12 of Article 378.2 of the Tax Code of the Russian Federation).

Once you have established the cadastral value, you can proceed to determining the tax base and calculating tax (advance payments).

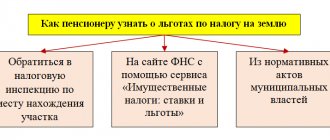

To find out where you can find out the required cadastral value, read the article “How to find out the cadastral value of property?” .

Attention! If the cadastral value is established by the court taking into account VAT, then the taxable base is the value of the property excluding tax. See details here.

What is the difference between a tax and a fee?

The differences between a tax and a fee are as follows:

- The fee is levied in connection with the payer's desire to have a certain right (license or permit). For example, a trade fee (collected only in Moscow, i.e. it is a local fee) for the right to use objects for trade.

- Fees are one-time in nature, and taxes are paid periodically.

- The purpose of collecting a fee is to compensate for additional budget expenses associated with the provision of specific public legal services to a specific payer.

Tax and reporting periods

The tax period for both taxes is one year (Articles 379, 405 of the Tax Code of the Russian Federation). There are no reporting periods for individuals. For legal entities, these are quarters if the base is the cadastral value of the property, and the first quarter, six months and 9 months if the tax base is the average annual value of the property. Therefore, unless the region has established otherwise, organizations need to pay an advance payment quarterly.

Taxes and special regimes

In addition to the previously discussed groups of taxes, the Tax Code of the Russian Federation identifies so-called special regimes, the use of which exempts from payment of income tax, personal income tax (for individual entrepreneurs), VAT, property tax of organizations and individuals, but introduces the obligation to pay a single tax.

Recommendations from ConsultantPlus experts will help you choose the optimal tax regime. You can view them by getting free trial access to the K+ system.

The following modes are distinguished:

- simplified tax system;

Read about the specifics of calculating and paying this tax in the “STS” section.

- regime for agricultural producers;

For materials on calculation, payment and reporting in this mode, see the “Unified Agricultural Tax” section.

- production sharing agreement;

- patent system.

The nuances of the patent taxation system can be found in the “PSN” section.

Let's look at the types of taxes and fees in the Russian Federation.

What determines the amount of tax and who can pay it?

In the case of real estate, the amount of tax depends on its cadastral value at the beginning of the reporting year (that is, preceding the year in which payment is made). If the cadastral value has changed during this year, this should be reflected in the final amount payable.

At the same time, different rules apply for different real estate objects (they are described in detail in Article 403 of the Tax Code of the Russian Federation). For example, the tax base for an apartment or part of a residential building is determined as its cadastral value, reduced by the cadastral value of 20 square meters of the total area of this apartment or part of the house. For a room the reduction is made by 10 square meters, for a residential building (entirely) - 50 square meters.

In the case of vehicles, the tax amount depends on their power.

If there is more than one real estate, vehicle or land plot, taxes are assessed on each of them, and separate receipts are sent. Only the owner can pay the tax.

Methods of paying taxes

There are several options for where to pay taxes. First of all, it is worth noting that the receipt can be received in paper form by mail and electronically on the Federal Tax Service website. To receive a paper receipt, you should contact the tax authority with a statement about the need to provide information on paper. If you are a user of the Federal Tax Service website, all receipts will be sent only electronically by default.

In addition, a paper receipt is not sent if the tax amount is less than 100 rubles or, due to benefits, the individual is completely exempt from paying tax.

The receipt must arrive before November 1st! If you haven't received the document, contact your tax authority and ask for information about how much you need to pay.

- With a paper receipt you can pay tax at a bank branch. All you need is a receipt.

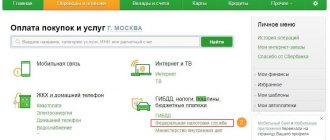

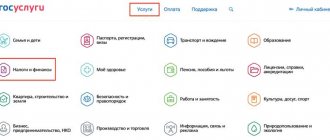

- Using an electronic copy, you can pay the tax through your personal account on the State Services portal or the Federal Tax Service website.

- You can use the State applications to pay using your phone.

List of federal, regional and local taxes in 2021 (table)

| Type of tax | Tax | Taxpayers | An object | Rates |

| Federal taxes | VAT The “VAT” section will help you understand the complex issues that arise when calculating, paying and reporting on this tax. | Art. 143 | Art. 146 | Art. 164 |

| Excise taxes Find answers to questions about what goods are excisable, what are the tax rates, and how to fill out a declaration in the “Excise Taxes” section. | Art. 179 | Art. 182 | Art. 193 | |

| Personal income tax How to calculate and withhold personal income tax, what deductions and benefits apply, how to prepare reports, see the “personal income tax” section | Art. 207 | Art. 209 | Art. 224 | |

| Income tax In the “Income Tax” section you can find all the news on the calculation, payment and submission of returns for this tax | Art. 246 | Art. 247 | Art. 284 | |

| Fees for the use of fauna and for the use of aquatic biological resources | Art. 333.1 | Art. 333.2 | Art. 333.3 | |

| Mineral extraction tax | Art. 334 | Art. 336 | Art. 342 | |

| Water tax In the materials of the “Water Tax” section, look for information about the list of objects of taxation, the nuances of calculating and paying the tax, as well as the timing of its transfer and rates | Art. 333.8 | Art. 333.9 | Art. 333.12 | |

| State duty | Art. 333.17 | Art. 336.16 | Art. 333.19, 333.21, 333.23, 333.24, 333.26, 333.28, 333.30, 333.31, 333.32.1, 333.32.2, 333.32.3, 333.33 | |

| Regional taxes | Organizational property tax You can read about the nuances of calculating property tax by organizations in the “Property Tax” section. | Art. 373 | Art. 374 | Art. 380 |

| Transport tax You will learn about the calculation procedure, possible benefits, and deadlines for paying transport tax from the materials in our special section “Transport Tax” | Art. 357 | Art. 358 | Art. 361 | |

| Gambling tax The specifics of calculating this tax are discussed in the section “Gaming Business Tax” | Art. 365 | Art. 366 | Art. 369 | |

| Local taxes | Property tax for individuals | Art. 400 | Art. 401 | Art. 406 |

| Land tax What it consists of, who should calculate and pay it, read in the materials of the section of the same name | Art. 388 | Art. 389 | Art. 394 | |

| Trade fee | Art. 411 | Art. 412 | Art. 415 |

Calculation of tax payment

The tax amount for the year is determined by the formula:

TnI = Tax base × Tax rate

If reporting periods and advance payments are established in your region, the payment for the reporting period (for example, for the 1st quarter) must be calculated based on ¼ of the cadastral value (share of cost) of the object (subclause 1, clause 12, article 378.2 of the Tax Code of the Russian Federation):

AP = Tax base × ¼ × Tax rate

In this case, the amount of tax payable at the end of the year will be equal to the difference between the calculated tax amount for the year and the amount of advance payments.

Example

The cadastral value of the property is 10 million rubles. The tax rate is 1.5%. Then:

- The annual tax amount will be 150,000 rubles. (10,000,000 × 1.5%);

- advance payments based on the results of the 1st quarter, half a year and 9 months will be equal to 37,500 rubles. (10,000,000 × ¼ × 1.5%);

- the amount of tax payable at the end of the year is RUB 37,500. (150,000 – 3 × 37,500).

However, if ownership of a real estate item arose or ceased during the reporting period, then the amount of tax for the tax period and advance payment for the reporting period is determined based on the number of full months of ownership. The formulas for calculation are:

- for advance payments:

AP = Tax base × ¼ × Tax rate × Number of full months of ownership of the property in the reporting period/3;

- for the full tax amount for the year:

NnI = Tax base × Tax rate / Number of full months of ownership of the property in a year / 12.

Starting from 2021, a full month of ownership is considered to be the one in which the right to the object arose before the 15th day or was lost after the 15th day (Clause 5 of Article 382 of the Tax Code of the Russian Federation).

EXAMPLE of calculation from ConsultantPlus, if the cadastral value has changed during the year: The organization owns a building that is taxed at the cadastral value. The tax rate in the region where this building is located is 2%. As of January 1, the cadastral value of the building was 100,000,000 rubles. In the spring, the organization dismantled a small part of the building, after which its area decreased. Information about the changed area was entered into the Unified State Register of Real Estate on June 10. After the changes, the cadastral value was determined to be 90,000,000 rubles. The organization will calculate property tax as follows... See . continuation of the example in K+. Trial access to K+ is free.

Insurance premiums

From 2021, Chapter was introduced into the Tax Code. 34, which provides for the payment of insurance contributions for pension, medical, social insurance for temporary disability and in connection with maternity (Law No. 243-FZ dated 07/03/2016). Until 2017, these contributions were paid to the budget of the Pension Fund and the Social Insurance Fund, respectively.

Payers of insurance premiums are listed in Art. 419 of the Tax Code of the Russian Federation, the object of taxation is specified in Art. 420, and the contribution rates are listed in Art. 425–430 Tax Code of the Russian Federation.

Find answers to questions related to the calculation, payment and reporting of insurance premiums in the “Insurance Premiums” section.

Object of taxation for corporate property tax

The object of taxation for corporate property tax is determined by Art. 374 Tax Code of the Russian Federation. According to the law, it is considered to be movable and immovable property, which is taken into account on the balance sheet of the taxpayer as a fixed asset.

IMPORTANT! Property tax must also be paid on property that the company has transferred for temporary use, trust management, or contributed to joint activities. The only nuance is who pays this tax.

For foreign organizations that operate through permanent representative offices, the object of taxation is the property that they received under a concession agreement. If a foreign company does not have a permanent representative office, then the tax is imposed on property located on the territory of the Russian Federation and owned by a foreign company, as well as property received under a concession agreement.

What cannot be subject to property tax? Land plots and other natural objects (lakes, forests), cultural heritage sites, nuclear installations, icebreakers, space objects, property of some federal bodies. Also, fixed assets belonging to depreciation groups 1 and 2 are not subject to tax. An example is an expensive printer for accounting needs.

Real estate in this case is something that cannot be moved: buildings, structures, objects of unfinished construction. Real estate transactions are subject to mandatory registration in the Unified State Register of Rights to Real Estate and Transactions with It. Movable property for property tax purposes - equipment, machines, automobile and cargo transport.

IMPORTANT! The legislation of different countries may classify the same object as real estate in one state, and as movable property in another. In such cases, the norm of the Civil Code (Article 1205) applies, according to which the belonging of an object to a certain type of property is determined according to the laws of the country where the object is actually located.

In the material “St. 374 of the Tax Code of the Russian Federation (2017): questions and answers,” our specialists have collected the most frequently asked questions regarding the determination of the object of property taxation and prepared detailed answers to them, taking into account the latest changes in legislation, letters from the Ministry of Finance, the Federal Tax Service and arbitration practice.

Results

The classification of taxes and fees in the Russian Federation consists of grouping them according to a certain criterion. The main one of these features is their grouping by budget levels. There are quite a lot of federal taxes. Due to the fact that they include such large taxes as income tax and VAT, the volume of federal taxes significantly exceeds the amount of fees to regional or local budgets.

Sources: Tax Code of the Russian Federation

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Object of taxation and tax base

The object of taxation is real estate that belongs to the taxpayer (Articles 374, 401 of the Tax Code of the Russian Federation). The tax base is the cadastral value of this property (Articles 375, 402 of the Tax Code of the Russian Federation). For individuals there is no alternative. For legal entities, if the object does not have a cadastral valuation, the average annual value is taken as the base, which is calculated according to accounting data. But there is less and less such real estate left.

What is cadastral value tax and what is its essence?

This is one of the types of mandatory payments to the state, which is based on an established tariff. A tax is generated and must be paid in a number of transactions with a house, apartment, etc. or at the end of the period.

The fixed tax on the cadastral value includes the determination of the latter - the price that is formed as a result of an independent assessment of the property. When calculating the total amount of the duty, the price is taken into account, which is formed according to methods approved by local authorities.

Important! To pay the correct fee, you need to obtain a certificate from the Unified State Register of Real Estate about the cadastral value (to order, follow the link).

When paying taxes based on the cadastral value, data from the unified register is taken into account. If they are not available, an independent initial assessment must be ordered.