Purchasing residential real estate in a new building has certain advantages, but there are some disadvantages and risks.

By buying an apartment from a reliable developer in a new building, a person receives a new home without a dark past and hidden owners. But you can end up with unscrupulous companies, especially if you refuse qualified legal assistance.

Compliance with all the details of a step-by-step transaction will eliminate the possibility of fraud. Let's take a closer look at the step-by-step instructions for purchasing an apartment in a new building with a mortgage.

Who issues the mortgage

When talking about a mortgage from a developer, many citizens do not quite correctly understand the mechanism for issuing a loan. It seems that since the program is “from the developer,” the mortgage is issued by the construction company itself. But this is not true at all.

A mortgage is a bank loan product. Banks cooperate with construction companies, and as part of this cooperation, mortgages appear for the purchase of new apartments and houses that have just been built or are still under construction.

That is:

- The developer is building.

- The bank issues a mortgage.

Previously, there were situations when the developers themselves offered buyers installment plans from themselves. They asked for a large down payment of 50% and spread the rest over 1 year. But now such offers have almost completely disappeared from the market.

Developers cooperate with banks, receive accreditation from them and offer mortgage loans to buyers. They often have separate employees who are authorized to accept applications and forward them to the bank. As a result, the purchase turns out to be as convenient as possible.

Nuances and possible problems when obtaining a mortgage

When applying for a mortgage, the main attention should be paid to the bank's conditions. The loan is provided for a period of up to 20 years. A long term looks convenient from the point of view that the obligatory monthly payment will be small, however, a long-term credit relationship with the bank is not the most desirable consequence. It is worth paying attention to whether there is a possibility of early repayment of the loan and how this happens. For example, some banks set a limit on the maximum monthly amount, which should not exceed 40% of the income of the borrower or co-borrowers.

Problems may also arise if the client does not have funds for the next payment. Some banks have a mortgage freeze feature that can be activated in the event of a job loss. Thus, the citizen suspends payments for a certain period - up to a maximum of 1 year. After which payment obligations are resumed.

It is also worth remembering that failure to pay a mortgage leads to loss of property. For non-payment of the loan, the bank has the right to sell the home at auction. If the apartment is sold at a cost exceeding the borrower's debt to the bank, the rest of the funds will be returned to him. However, apartments at auction often lose almost half of their original value. If even after the sale of the apartment the bank remains at a loss, it has the right to make up the costs by selling other property of the mortgagee.

Bank selection

If you have chosen a specific developer and one of his residential complexes or houses, you need to look at which banks have accredited this property. Accreditation is a complete check of the bank and the facility itself for legal purity. If the property is accredited, the bank issues mortgages for the purchase of apartments there and accepts them as collateral.

For the borrower, accreditation is a big plus; he can be confident in the cleanliness of the facility and the company that is constructing it. The bank's lawyers have already conducted a thorough analysis and declared the transaction safe.

The downside is that properties are often accredited by one or two banks, which greatly narrows the choice of credit institutions. But usually we are talking about large banks with good conditions.

It’s easy to find which banks have accredited the object of interest. All you have to do is go to the developer’s website, select an object and look at the terms of purchase. We need a “mortgage” section.

For example, on the website of the large company Donostroy, which is building residential complexes including in Moscow, the list of partner banks consists of a dozen items:

Moreover, each specific construction project undergoes separate accreditation by partner banks. For example, if you go to the bank section, you can see which properties of a particular developer it has accredited.

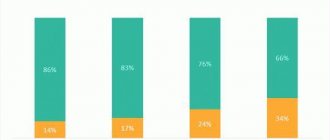

Here is the data for Donstroy and Gazprombank:

If you have already chosen a house or residential complex to purchase, go to the developer’s website in the section for this object and see the loan programs available for it. For example, here are the programs for the Symbols residential complex in Moscow from Donstroy:

The websites of other construction companies operate on the same principle of posting and providing information. There you will find all the information about partner banks and you can immediately apply for a mortgage.

How to obtain a mortgage for an apartment?

The procedure for registering ownership of an apartment in a new building with a mortgage requires the developer to:

- passing the acceptance of the object by the state architectural and construction commission;

- registration of commissioning of a new building;

- registration in the BTI of a technical passport for the constructed apartment building;

- registering an object for cadastral registration;

- drawing up a protocol on the distribution of real estate;

- registering the house in Rosreestr, assigning it a postal address.

Next, the developer provides the property owner with:

- act of acceptance and transfer of housing;

- act of implementation of an investment agreement for construction work;

- copies of documents stating that the house was put into operation and the state commission accepted it.

The received papers should not contain corrections, additions, or errors, otherwise such documents will not be accepted by the registrar (Law No. 122-FZ). If the developer refuses to issue any of the papers or diligently delays the issuance process, you can demand them through the court.

The owner orders from BTI:

- technical and cadastral passport;

- floor plan.

The following are submitted to Rosreestr or MFC:

- owner passports;

- DDU agreement or other agreement with the developer;

- mortgage agreement;

- written consent of the bank to own and use the collateral;

- all the above papers that were requested from the developer and from the BTI;

- receipt of payment of state duty.

The organizations take all originals and copies and issue a receipt. If everything is fine with the documents, the procedure will last 10-18 days. Refusal to register can be appealed through court.

Next, a document on ownership will be issued, there will be a note indicating that the apartment is encumbered with collateral. After full payment of the mortgage, the removal of the encumbrance is registered in Rosreestr.

Registration

The term "registration" is no longer used. It was replaced by the term "registration". When can I register? After registration of ownership.

Purchase option #1. Through the developer

Every major construction company has an office to accept applications for mortgage programs. Representatives of the developer work there, trained by banks and given access to the program for accepting mortgage applications.

If a company works with a large number of banks at once, it can create a special single brokerage form for accepting applications. As a result, for example, if a buyer has chosen an apartment in a building that has been accredited by Sberbank, VTB and PSB, the application will be sent directly to these three banks. It's comfortable.

How is such a mortgage obtained from the developer:

- Studying the property, choosing an apartment, booking it.

- A visit to the brokerage department of the developer with primary documents (only a passport or passport + certificates, the manager will tell you exactly). Applying for a mortgage.

- An automatic response from the bank or banks may occur almost immediately. If there are several approvals, the buyer chooses the best option.

- The developer prepares a package of documents for the bank, which includes the client’s documents and papers for the property being purchased. The bank conducts an inspection within 2-3 days.

- If there are no complaints, final approval is given for the purchase of a specific object, and a payment schedule is drawn up.

- The borrower visits a bank branch, signs a loan agreement, and buys mandatory insurance. Next, the transaction is registered in Rosreestr. If the property is still under construction, ownership will arise after the delivery of the house.

This method of obtaining a mortgage from a developer can be called the most convenient, since the paperwork and dialogue with the bank is taken over by the construction company.

Step-by-step registration process

If a future borrower chooses a specific property and housing, he must go through the following steps:

- collects all necessary documents for obtaining a mortgage;

- submits an application for a loan (either himself or through a mortgage broker from the developer);

- signs the agreement with the developer (after the bank approves the procedure);

- signs mortgage documentation at the bank;

- registers the transaction;

- pays the down payment to the developer;

- the bank transfers the money to the developer.

If you purchase an apartment in a building under construction, the bank always pays attention to the completion date of construction. The home remains the property of the financial institution as long as the borrower pays off the mortgage.

Read more about how the purchase takes place below.

More about the process

The future borrower has chosen the property that he is going to buy under a mortgage agreement. Next you need to decide on a developer.

The closer the property is to the completion date, the higher the cost of the apartment. That's why many people buy apartments that don't actually exist yet. As mentioned above, the most dangerous deal is when only a foundation pit has been dug.

According to many realtors, the most profitable investment is purchasing real estate in a property that is already 70% ready. This means that the house has been built, but is not yet ready for delivery, and finishing work is underway.

The risk of construction freeze is reduced. Also, at this stage, the cost of apartments has not yet risen to its maximum.

You need to book the option you like with the developer by concluding an agreement. The document specifies the characteristics of the property, the presence or absence of certain problems, the terms of purchase, and the amount of the down payment. When applying to a bank for a mortgage, you must show this agreement.

Documentation

The developer must be required to provide all the following documents:

- certificate of ownership of the land plot and the facility being built on this land;

- a construction permit issued by a government agency;

- act of distribution of apartments;

- investment contract.

Documents submitted to the bank:

- passport of a citizen of the Russian Federation;

- a copy of the work book;

- income certificate;

- investment agreement drawn up together with the developer;

- copy of the tax return;

- a copy of the developer's decision to sell the apartment.

Each credit institution may require any additional documents . The bank reviews the application and documents, and then contacts the client, informing about the approval of the application or refusal. Then a mortgage agreement is drawn up.

As soon as the mortgage is issued, the apartment will become the property of the borrower under a purchase and sale agreement. The transaction is formalized in Rosreestr.

Typically, a mortgage is issued within a month. During this period the money is transferred. If the mortgage agreement is concluded, but the house has not yet been rented, the reservation agreement will remain in force for some time.

But what to do after receiving the keys? Receiving the keys to a new apartment is a joyful moment, especially if the apartment was purchased in a new building during the construction stage. But the full owner of the home will be the one who registers ownership of the apartment.

Purchase option No. 2. Independent application to the bank

You can also get a mortgage for a new property by contacting the bank in person. And here there are two options for the development of events:

- First, select an object, look at the list of banks that have accredited it and submit applications for a mortgage. The easiest way to do this is online; all banks accept requests this way and even reduce rates for it.

- First, choose a bank, and then look on its website which objects it has accredited. If approved, choose any house or residential complex from this list.

The registration process itself is identical to the first option, you just have to run around a little more. Here it is no longer the developer’s representative who handles the paperwork, but the borrower who carries the documents from the developer to the bank. But in any case, the construction company will help you collect documents and prepare everything.

Banks practically do not issue mortgages for unaccredited properties. It's too risky for them. And if you find such a bank, you will have to collect a huge set of documents for the developer and the house.

Features of the acquisition

Where to start buying a new apartment with a mortgage? When contacting a bank, the future owner of an apartment will inevitably encounter a number of features:

- when selecting residential real estate, you need to contact only accredited construction organizations that the bank can trust;

- mortgage funds will be issued if construction is in its final stage;

- the mortgage will be issued only for a project that has passed state registration (the borrower must secure the transaction, for example, provide property as collateral).

First you need to decide which house to buy a home in . If a decision has been made to purchase an apartment in a building under construction, there are several acquisition options:

- Equity Participation Agreement (EPA). It is concluded immediately with the developer. After completion of construction, the owner will receive a registration certificate and become the full owner of his property (here you need to rely on Law 214-FZ).

- Agreement of assignment or assignment. The apartment will be purchased from the investor. Disadvantages: the state actively supports developers, and the interest rate for housing purchased under an assignment agreement is much higher than for an apartment purchased from a developer. After the house is handed over and accepted by the state commission, assignment is impossible.

- According to the agreement of the housing construction cooperative. Experts say this is an unsafe method. This sales option does not exclude a double sale.

- Under a preliminary purchase and sale agreement. The document is concluded only if the house is handed over, but there are no documents confirming ownership yet.

Next, we’ll look at how to get a mortgage for a new building.

Purchase from a developer

To purchase real estate from a construction company, you must follow certain steps. What you need to know:

- First, decide on the area where you are going to live.

- Very often, the purchase occurs at the construction stage of an apartment building. Such housing is usually sold with a rough finish, and it will not be possible to move into it quickly. Repair needed.

- Before choosing a particular property, a person must carefully study the property itself, the developer, the bank’s conditions, and then enter into an agreement. Then the parties sign the transfer and acceptance certificate, the buyer receives the keys and registers the property. The most unsafe option for purchasing mortgaged housing is the foundation pit stage.

Mortgage conditions from the developer

The developer himself cannot dictate the terms of the mortgage loan; they are created by the bank. But within the framework of partnership agreements, special programs with extremely competitive rates can be created.

The main conditions are:

- availability of a down payment of at least 10-20%. Without a down payment, a mortgage from the developer will not be issued. An exception is that some banks allow the use of maternity capital as investment capital;

- The borrower has an official job, with at least 3 months of experience. The level of income and the fact of employment are confirmed by certificates;

- the borrower has reached 21 years of age. Each bank has its own age limit at the time of full repayment of a mortgage; look at the requirements for the borrower; sufficient solvency to repay the mortgage;

- you can apply all the required subsidies, complete a Family Mortgage transaction, and use maternity capital;

- The purchased object must be insured for the entire loan repayment period.

If a mortgage from a developer is taken out by spouses, they become co-borrowers and bear identical responsibility for repayment. The second party to the transaction also carries documents, but there is no requirement for mandatory employment.

Give your rating

What additional steps are possible in obtaining a mortgage?

The procedure for obtaining a mortgage is quite stable, so there will be no deviations from the above stages. However, for some citizens, this stage may involve collecting the documents necessary to submit an application. This step is necessary in any case, but the set of documents may vary. For example, sometimes the bank does not require official confirmation of income, but due to this “bonus” it increases the overall interest rate on the loan.

Also, in some cases, the bank may additionally require an updated income certificate. This happens if the client was unable to choose a suitable apartment within the 3 months allotted to him. The reason for updating the certificate may also be other situations due to which the procedure for obtaining a mortgage has been delayed.

Sometimes, in order to reduce mortgage rates, citizens are advised to prepare the ground” at the bank. The most favorable conditions are offered to current bank clients, so it is recommended to apply to banks whose cards have been issued. However, priority is given to salary card holders, since monthly transfers will serve as additional confirmation of the borrower’s income. Some banks offer discounts for meeting certain requirements. For example, Sberbank reduces the mortgage rate with electronic registration.

FAQ

Mortgage from the developer, what is it?

This is a mortgage issued by a bank for the purchase of an apartment in a building under construction or already built, or for the purchase of a private house from a developer. The seller can only be an accredited developer.

Why is a mortgage from a developer better than a secondary one?

Interest rates for such programs are traditionally lower. In addition, you are buying a new property verified by the bank - the buyer’s risks are reduced to zero.

Is it possible to get a mortgage from a developer without certificates?

If the bank you choose gives you this opportunity, then it’s possible. For example, there are such offers in Sberbank and Alfa-Bank. But the stakes for such simplified proposals are rising.

Is it possible to buy an apartment from an unaccredited developer through Sber?

No, Sberbank accepts only accredited objects as collateral, a list of which can be found on the Domklik website.

What should I do if two banks available to me refused?

This means that you will not be able to buy this property with a mortgage. Choose another one with different banks or consider a secondary facility. In the latter case, you can apply for a mortgage at any bank.

about the author

Irina Rusanova - higher education at the International East European University in the direction of "Banking". Graduated with honors from the Russian Economic Institute named after G.V. Plekhanov with a major in Finance and Credit. Ten years of experience in leading Russian banks: Alfa-Bank, Renaissance Credit, Home Credit Bank, Delta Credit, ATB, Svyaznoy (closed). He is an analyst and expert of the Brobank service on banking and financial stability. [email protected]

Is this article useful? Not really

Help us find out how much this article helped you. If something is missing or the information is not accurate, please report it below in the comments or write to us by email

Where to start designing

Banks, trying to take into account possible risks, put forward requirements for potential borrowers. The client should evaluate his financial capabilities. Attention should be paid to the following factors:

- Age

. You can take out a loan for real estate from the age of 21. Banks rarely sign contracts with students who cannot yet fully devote themselves to work. Also, financial and credit organizations are wary of pensioners. With rare exceptions, banks strive to ensure that the borrower is no more than 65 years old at the time of repayment of the mortgage.

- Financial situation

. The minimum down payment amount is usually 10 – 15%. It is also important for the bank to make sure that the client’s income is enough for monthly payments. It is more profitable for a financial institution to provide loans to families in which both spouses have a permanent job.

- Seniority

taken into account when purchasing an apartment or house with a mortgage. The client must work in one place for at least six months.

It is advisable to repay previous loans in full in order to increase the chances of approval of a new one.

Comments: 0

Your comment (question) If you have questions about this article, you can tell us. Our team consists of only experienced experts and specialists with specialized education. We will try to help you in this topic:

Author of the article Irina Rusanova

Consultant, author Popovich Anna

Financial author Olga Pikhotskaya

We collect a package of documents

So, you have decided to take out a home loan. But how to get a mortgage, where to start? The standard list of documents is the same for different banks, but there are some peculiarities. It is necessary to study the requirements of a particular institution on the website, by phone or during a personal visit. Here's what's included in the basic package:

- borrower's passport;

- insurance certificate;

- data on marital status;

- information about the borrower’s income (certificate 2-NDFL);

- a copy of the work book.

Often financial and credit institutions ask to provide evidence of additional sources of income and profit. Documents confirming income to the family budget will only be a plus.

Should I contact an agency or realtor?

The question of engaging a realtor as an assistant in the selection of housing options in the non-primary market remains open. Everyone decides for themselves how important the advice of another person is to him for an additional fee. However, we should not forget that a serious agency usually offers not so much a guide to houses under construction and semi-finished objects, but rather legal assistance in choosing a developer and a profitable credit plan.

It’s definitely worth paying an intermediary if:

- a person buys real estate in another city unfamiliar to him;

- the client does not have the opportunity to choose options that fit his criteria;

- the agency has a lawyer on staff who is ready to explain the provisions of the contracts proposed for signature;

- the realtor is ready to take upon himself not only the selection of objects, but also their verification (analysis of the reliability of the developer, obtaining extracts from the Unified State Register of Real Estate, reviewing information about debts and encumbrances).