Utility payment period

As noted above, payment for housing and communal services is carried out on the basis of payment documents provided by the contractor. They are compiled using data from metering devices installed in residential premises or houses.

Payment deadlines are established:

- based on the current requirements of legislative acts, namely Article 155 of the Housing Code of the Russian Federation and Article 66 of the Resolution of the Russian Government. They prescribe the need for a citizen to pay fees for the provision of housing and communal services no later than the 10th day of the month following the reporting month;

- on the basis of an agreement valid between the citizen and the provider of housing and communal services. Contractual terms may differ from those specified in the regulations above. In most cases, they are longer than those established by the Housing Code of the Russian Federation and the Decree of the Russian Government.

In case of failure to comply with the payment deadlines specified in the contract for the provision of one or another housing and communal services, the legislation provides for quite serious penalties. Their size is 1/300 of the refinancing rate established by the Central Bank of the Russian Federation. In case of partial payment, the amount of the remaining debt is taken into account in calculating the penalty.

What to do if there is no payment

There is no need to panic, nor should you call social security for no reason, which already receives hundreds of similar calls every day.

First of all, you need to think about why the funds might not have arrived in your account. So, payment could be suspended, and there are many reasons for this. You have to wonder if one of them was:

- the expiration of the terms for which the benefit was assigned;

- card blocking or problems with book maintenance;

- failure to pay utility bills for two months.

Having considered the most probable reasons and ruled them out, call social security, where they can clarify the situation for you. In most cases, you can simply fix the problem and continue receiving funds, receiving them even for the month for which you did not want to provide them. Or the problem will be eliminated by social security itself, if a mistake was made on its part. In general, most problems are resolved peacefully, unless there are serious violations due to which the accrual of funds was stopped.

Sometimes it happens that money is credited, but does not arrive in the account. In such a situation, there is also no need to be afraid. You just need to take the statement about the provision of money and send it to the bank, where they will double-check everything and fix the problem. In addition, sometimes accrual is suspended for some period due to technical problems, usually by the bank, and after a day or two the money arrives.

This is rare, but it also happens. Technical failures sometimes lead to money hanging in the air, but contacting bank specialists allows you to quickly resolve the issue and receive the funds due.

Confirmation of payment of utilities

In recent years, various systems using online services, various bank cards and virtual wallets are increasingly used when making payments for housing and communal services. In this case, conflicts and controversial situations often arise between the organization that provides services and the citizen receiving them. This becomes possible if one of the parties makes an error either when making a deposit or when processing a payment.

In order to avoid possible conflict situations, it is necessary:

- When paying for utility bills in cash, always keep all supporting documents. In this case, as a rule, there are no problems with proving the execution of the payment;

- When using various payment systems, bank cards, ATMs or electronic wallets, you should carefully follow the instructions for their use. Most systems provide a citizen with the opportunity to print out receipts confirming the deposit of funds and containing all the necessary details for proof.

It should be understood that if the situation is brought to court, it will be extremely difficult to cope without the help of a qualified and practicing lawyer. Therefore, you should always promptly check the progress of the payment and reconcile with housing and utility service providers as often as possible.

Dependence on the time of submission of documents

When considering the issue of the deadline for submitting documents, it should be noted that it is important for determining the period for which subsidies will be provided.

So, if you manage to submit the papers before the 15th day of the current month inclusive, you can count on receiving compensation for this month.

But if you submit the papers on the 16th or later, then payments can only be expected from the next month, but the subsidy will be issued immediately in two months, that is, you will not lose your funds.

The countdown of the period for receiving compensation will also begin from the month in which you submitted the papers, since you will still receive money for it.

Important! Subsidies are assigned only for six months, in some regions - for a year. Having received payments for this period, you must resubmit documents if you expect to continue receiving assistance for housing and communal services. If you do not submit the paperwork again, the funds will simply stop flowing into your account.

Checking utility bills

There are several main ways to check whether you have a debt or whether payments have been made for various utility services. The most traditional method - a direct visit or telephone call to the service provider - is increasingly rare. This is not surprising, since it is time-consuming and quite inconvenient from the point of view of obtaining clear and timely information.

In recent years, various Internet systems have been increasingly used. Their number is constantly increasing. Therefore, experts in the field of information technology recommend that citizens work with the most proven and proven resources. Moreover, these can be both the sites of the housing and communal services providers themselves, as well as specialized organizations that offer the possibility of paying for them - banks, intermediaries, etc.

In Moscow, the most popular system is the Unified Payment Document (UPD), provided by the official portal of Moscow city services. It contains information about all types of housing and utility payments that a citizen is required to make. Considering the success of this system, it is likely that similar portals will be created for other regions of Russia.

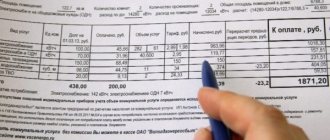

Photo No. 2. ENP website

Compensation for utility costs: the position of the Ministry of Finance

Relations between the parties when leasing property are regulated by Chapter 34 of the Civil Code. Under a lease (property lease) agreement, the lessor (lessor) undertakes to provide the lessee (tenant) with property for a fee for temporary possession and use or for temporary use. This definition is given in Article 606 of the Civil Code. At the same time, the tenant is obliged to maintain the property in good condition, as well as bear the costs of maintaining this property, unless otherwise established by law or the lease agreement (clause 2 of Article 616 of the Civil Code of the Russian Federation). Such expenses, in particular, include utility costs, the amount of which varies from month to month.

Polukhina M.Yu. General provisions

At the same time, the amount of rent may be changed by agreement of the parties within the time limits specified in the contract, but, in accordance with paragraph 3 of Article 614 of the Civil Code, no more than once a year. For this reason, in practice, most often, under a lease agreement, the tenant compensates the landlord for a share of the cost of the utilities consumed by him separately from the rent. The landlord directly enters into contracts with organizations that provide utility services. They, in turn, provide the lessor with primary documents for their services on a monthly basis, and also issue invoices. The total cost of utilities is determined by their actual consumption based on bills issued by utility services.

The share of the tenant's expenses compensated by him under the lease agreement can be determined in different ways:

- the amount of actually consumed utilities is calculated as a percentage of the occupied rental space of the premises;

- the amount of electricity consumed is determined by the readings of individual meters;

- energy consumption is determined based on the power of the partners’ equipment and its operating time.

In any case, the calculation method must be fixed in the lease agreement.

Tax accounting

Electricity costs

The question arises about the procedure for carrying out these services for both the landlord and the tenant in tax and accounting.

In this regard, the opinion of the Ministry of Finance of Russia, published in the recently published letter of the Federal Tax Service of Russia dated April 23, 2007 No. ШТ-6-03/ [email protected] , on the procedure for applying value added tax in relation to funds transferred by the tenant to the landlord for compensation purposes is interesting the landlord's expenses for paying for utilities, communication services, as well as security and cleaning services for the rented premises under agreements under which these expenses are not included in the cost of renting the premises.

Thus, the letter of the Ministry of Finance of Russia dated 03.03.2006 No. 03-04-15/52 sets out the position on the application of VAT in relation to the amounts transferred by the tenant to the landlord in order to compensate the landlord’s expenses for paying for electricity. In particular, it states that the lessor has no reason to classify operations for the supply (supply) of electricity under these contracts as operations for the sale of goods for VAT tax purposes. Therefore, these transactions are not subject to VAT taxation; invoices for electricity consumed by the tenant are not issued by the landlord.

The Ministry of Finance of Russia bases this statement on subparagraph 1 of paragraph 1 of Article 146 of the Tax Code, from which it follows that the object of taxation with value added tax is transactions involving the sale of goods (work, services), as well as the transfer of property rights on the territory of the Russian Federation.

In addition, it is noted that according to paragraph 1 of Article 539 of the Civil Code, under an energy supply agreement, the energy supplying organization undertakes to supply energy to the subscriber (consumer) through the connected network, and the subscriber undertakes to pay for the received energy, as well as to comply with the regime of its consumption stipulated by the agreement, to ensure the safe operation of those in its management of energy networks and the serviceability of the instruments and equipment used by it related to energy consumption. The subscriber in this case is the person on whose balance sheet the energy consuming object is listed.

The lessor is not an energy supplying organization for the tenant, since he himself receives electricity as a subscriber (Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated April 6, 2000 No. 7349/99).

Based on the foregoing, it is noted that the tenant compensates the landlord’s expenses for paying for electricity and does not receive an invoice for the electricity he consumes, therefore he does not have the right to deduct the VAT amounts transferred by him to the landlord as part of the compensation amounts.

But the landlord also faces difficulties in accounting for VAT on utilities. The Ministry of Finance, referring to the provisions of Article 170 of the Tax Code, notes that VAT amounts charged to the buyer when purchasing goods (work, services) in the case of their use for transactions not subject to VAT are not deductible. Consequently, the lessor is not subject to deduction of VAT on electricity charged to him by the energy supply organization in relation to the electricity consumed by the tenant.

...and all other utility bills

In letter dated March 24, 2007 No. 03-07-15/39, the Ministry of Finance of Russia went even further in its reasoning, extending the above point of view on the application of VAT in relation to funds transferred by the tenant to the landlord in order to compensate for the landlord’s expenses for payment not only for electricity, but also for all utilities, communication services, as well as security and cleaning services for rented premises under contracts according to which these expenses are not included in the cost of rental services.

However, a completely different point of view on this issue is expressed by the Federal Tax Service of Russia for the Moscow Region in its letter dated 02/03/2005 No. 21-27/28632 (hereinafter referred to as the letter of the Federal Tax Service for the Moscow Region). It is based on the fact that when determining the tax base for VAT, revenue from the sale of goods (work, services) is determined based on all the taxpayer’s income associated with payments for the specified goods (work, services) (Clause 2 of Article 153 of the Tax Code of the Russian Federation) . According to subparagraph 2 of paragraph 1 of Article 162 of the Tax Code, the tax base is increased by amounts received for goods (work, services) sold in the form of financial assistance, to replenish special-purpose funds, to increase income, or otherwise related to payment for goods (work, services) sold ).

From this it is concluded that the funds received by the landlord from the tenant in the form of compensation for the cost of utility bills (energy supply, heat supply, water supply, etc.), in the part consumed by tenants, are subject to VAT. Consequently, VAT amounts paid by landlords to utility service providers, including the part consumed by tenants, are deductible from the landlord on the basis of Articles 169, 171, 172 of the Tax Code. The tenant can also deduct VAT on specified expenses (compensated to the landlord) only on the basis of invoices.

However, a later letter from the Federal Tax Service of Russia dated December 29, 2005 No. 03-4-03/2299/ [email protected] “On the procedure for applying the 0 percent VAT rate” states that the landlord in this situation has no grounds for issuing appropriate invoices -invoices, and the tenant has the right to VAT refund.

To date, tax authorities refuse to express and comment on their point of view on this issue.

What about expenses?

Also very interesting is the question of including in the expenses taken into account for the purpose of calculating profits the costs of paying the above expenses.

The Ministry of Finance of Russia, in letter dated August 4, 2005 No. 03-03-04/2/41 “On accounting for utility bills when subleasing property,” expressed the following point of view. Referring to subparagraph 10 of paragraph 1 of Article 254 of the Tax Code, he confirmed the tenant’s right to take into account as other expenses expenses associated with the payment of utility bills and (or) communication services related to premises leased. The sublessee may also take into account, as part of other expenses associated with production and sales, the costs of payment of utility and operating expenses incurred by him under the sublease agreement. In this case, the tenant, when receiving rental and utility payments from the subtenant, takes these amounts into account as part of other expenses (clause 4 of Article 250 of the Tax Code of the Russian Federation). Despite the fact that the letter speaks of sublease relations, the opinion reflected in it is also valid for relations arising between the tenant and the landlord.

The opinion of the tax authorities on the issue of calculating profit is set out in the above-mentioned letter from the Federal Tax Service for Moscow Region. It states that if the tenant reimburses the landlord for the costs of maintaining and operating the leased property (utility expenses) provided for in the lease agreement, then these payments are reflected by the lessor as part of non-operating income or income from sales, while for the tenant - as part of non-operating expenses.

If a separate agreement is concluded between the parties for reimbursement of the above expenses, these payments are taken into account by the lessor as part of sales income on the basis of paragraph 2 of Article 249 of the Tax Code. For the lessee, these payments are not recognized as expenses for profit tax purposes.

As for utility bills, these expenses, in accordance with subparagraph 5 of paragraph 1 of Article 254 of the Tax Code, are taken into account as part of the material expenses of the party that has entered into direct contracts with organizations that provide utility services. This is very important, since in this situation the tenant does not have direct contracts with utility services and will not be able to include in expenses the amount of utility bills reimbursed to the landlord.

But in later letters from the Federal Tax Service in Moscow dated July 6, 2005 No. 20-12/47837, as well as dated June 26, 2006 No. 20-12/56637 and dated June 28, 2006 No. 19-11/ 58877 expresses a point of view similar to that of the Ministry of Finance.

These letters indicate that if the lease agreement provides for obligations to pay actually consumed utility costs and expenses for communication services for the tenant, he includes these expenses as part of material and other expenses associated with production and (or) sales. In this case, the condition of validity and documentary confirmation of these expenses with primary documents must be met in accordance with paragraph 1 of Article 252 of the Tax Code. It also provides a list of these documents: the landlord's invoices, compiled on the basis of similar documents issued to the landlord by public utilities, in relation to the actual use of these services by the tenant.

The lessor, in turn, has the right to include as expenses amounts transferred to organizations providing utilities and communication services.

Accounting

All of the above concerns tax accounting. Now let's look at this situation within the framework of accounting using the following example.

Example 1

provides for rent warehouse space owned by it. According to the lease agreement, the tenant compensates her for 10 percent of the cost of utilities separately from the rent. The cost of utilities is calculated based on their actual consumption according to invoices issued to the landlord by the relevant utility services, and amounts to RUB 70,800 for July 2007. (including VAT – 10,800 rubles). The share is equal to 7,080 rubles. (including VAT - 1,080 rubles). The rent is 17,700 rubles. (including VAT - 2,700 rubles) A document and an invoice were provided to the tenant. Calculations are made monthly.

Rent and utility reimbursement amounts for July were transferred on August 9, 2007.

Providing space for rent is the main activity. For the purpose of calculating profits, firms operate on the accrual basis.

It should be noted that in order to avoid disputes with the tax authorities, the landlord in the invoice issued to the tenant does not indicate in the text “Payment of utilities.

The following entries will be made in the lessor's accounting:

July 31, 2007:

Debit 20 Credit 60 – 54,000 rub. ((RUB 70,800 – RUB 10,800) – (RUB 7,080 – RUB 1,080) – reflects the cost of the landlord’s utility expenses;

Debit 19 Credit 60 – 9,720 rub. (RUB 10,800 – RUB 1,080) – reflects part of the VAT amount presented by utility services on the basis of invoices in relation to services consumed by the lessor;

Debit 68 Credit 19 – 9,720 rub. – the amount of VAT corresponding to the costs of utilities consumed by the lessor is accepted for deduction.

At the same time, in the purchase book, the company does not record all amounts for received invoices for utilities, but only the amounts consumed specifically by it, that is, 9,720 rubles.

Debit 60 Credit 51 – 70,800 rub. – payment for utilities has been made;

Debit 76 Credit 90-1 – 15,000 rub. (RUB 17,700 – RUB 2,700) – rent accrued for July 2007;

Debit 90-3 Credit 68-2 – 2,700 rubles. – VAT has been charged on the rental amount;

Debit 76 Credit 60 – 7,080 rub. – the tenant is presented with the amount of utility costs to be reimbursed.

August 9, 2007:

Debit 51 Credit 60 – 24,780 rub. (RUB 17,700 + RUB 7,080) – the amount of rent and compensation for utility costs was received from the tenant.

In tax accounting, as was said, rent can be accepted as income from the main activity with VAT charged on these amounts to the budget. The amount of utility payments compensated under the lease agreement is not accepted by it as income for the purpose of calculating profit. It is not subject to VAT, as it is not a sale.

Let's look at accounting as a lessee.

The company's accounting department will make the following entries:

July 31, 2007:

Debit 20 (25, 26, 44) Credit 76 – 15,000 rub. (RUB 17,700 – RUB 2,700) – rent for July 2007 is reflected;

Debit 19 Credit 76 – 2,700 rub. – the amount of VAT on rent is reflected in accordance with the agreement;

Debit 68 Credit 19 – 2,700 rub. – the amount of VAT on rent is accepted for deduction.

We remind you that the landlord issues an invoice to the tenant for the amount of compensation for utility bills without allocating the amount of VAT, as well as copies of utility bills. , the tenant, reflects the entire amount of the utility bill in expenses both in tax and accounting, without independently allocating VAT.

Debit 20 (25, 26, 44) Credit 76 – 7,080 rub. – reflects the cost of utility expenses subject to reimbursement to the lessor for July 2007.

August 9, 2007:

Debit 76 Credit 51 – 24,780 rub. (RUB 15,000 + RUB 2,700 + RUB 7,080) – the rent and the amount of reimbursed utilities are transferred to the lessor.

How to solve a problem?

To avoid controversial issues in accounting with the tax office, some companies simplify contractual relations when leasing premises. The amount of the cost of rental payments under the contract includes the amount of compensation reimbursed to the lessor for utilities, communication services, as well as security and cleaning services. In this case, the specified amounts are reflected by the lessor as part of non-operating income or income from sales, subject to VAT. The tenant has the right to take them into account as non-operating expenses, and also to deduct VAT amounts on them based on the invoice issued by the lessor.

There is another way to solve this issue. It is also associated with the appropriate execution of contractual relations between the parties to the lease agreement. Its essence is as follows. It must be clear from the lease agreement concluded by the parties that the lessor, when paying for services to public utilities, acts on his own behalf, but at the expense of the tenant. The content and form of the agreement must correspond to intermediary agreements. In particular, a commission agreement defined in Chapter 51 of the Civil Code of the Russian Federation, or an agency agreement in accordance with Chapter 52 of the Civil Code of the Russian Federation. In this case, the landlord re-issues invoices from utility organizations to the tenant, highlighting VAT amounts.

In order to accept the amounts of “input” VAT for deduction, the landlord, acting as an intermediary between the tenant and utilities, must issue invoices on his behalf for the amounts of utility payments. This explanation was given in the letter of the Ministry of Finance of Russia dated November 14, 2006 No. 03-04-09/20.

In addition, in accordance with the provisions of the Civil Code, the landlord is entitled to remuneration for intermediary services. To avoid additional costs on the part of the tenant, the parties can agree to reduce the rent by the amount of the remuneration.

Based on the documents received, the tenant has the right to deduct the VAT amounts paid to the landlord and also reflect them in the purchase book.

Let's look at this situation using an example.

Example 2

Let's return to the condition of the previous example. With the only change that in terms of utility costs, the tenant is a commission agent and acts before utility organizations on his own behalf, but on behalf of; upon receipt of invoices from utility services, reissues them to the tenant with the allocation of VAT amounts, and also issues invoices for the specified amounts on its own behalf. In addition, acting as a commission agent in this transaction, he receives a remuneration of 1,770 rubles. (including VAT - 270 rubles).

The parties agreed to reduce the monthly rent by this amount. submits the commission agent's report, a certificate of completion of work and an invoice for his remuneration.

The following entries will be made in accounting:

July 31, 2007:

Debit 20 (25, 26, 44) Credit 76 – 13,500 rub. (RUB 15,930 – RUB 2,430) – rent for July 2007 is reflected;

Debit 19 Credit 76 – 2,430 rub. – the amount of VAT on rent is reflected in accordance with the agreement;

Debit 68 Credit 19 –2,430 rub. – the amount of VAT on rent is accepted for deduction;

Debit 20 (25, 26, 44) Credit 76 – 1,500 rub. (1,770 rubles – 270 rubles) – reflects the commission agent’s remuneration () for services performed;

Debit 19 Credit 76 – 270 rub. – the amount of VAT on commission fees is reflected;

Debit 68 Credit 19 – 270 rub. – the amount of VAT on commission remuneration is accepted for deduction;

Debit 20 (25, 26, 44) Credit 76 – 6,000 rub. (7,080 rubles – 1,080 rubles) – reflects the cost of utility expenses subject to compensation to the lessor for July 2007 based on his invoice;

Debit 19 Credit 76 – 1,080 rub. – reflects the amount of VAT on utility payments on invoices reissued by the lessor;

Debit 68 Credit 19 – 1,080 rub. – the amount of VAT on utility bills has been accepted for deduction.

The amount of VAT in the amount of RUB 1,080 indicated in the invoices received from the landlord for utility costs, as well as the VAT amount on rent in the amount of RUB 2,430. and the amount of VAT on commission in the amount of 270 rubles are reflected in the purchase book.

August 9, 2007:

Debit 76 Credit 51 – 24,780 rub. (13,500 rubles + 2,430 rubles + 1,500 rubles + 270 rubles + 7,080 rubles) – the rent, commission and the amount of reimbursed utilities to the lessor are transferred.

In excess of the rent

Readers should pay attention to the latest letter of the Ministry of Finance of Russia dated June 19, 2007 No. 03-11-04/2/166.

It addresses the situation when, in accordance with the terms of the lease agreement, the cost of communication services by the tenant is paid in addition to the rent. The Russian Ministry of Finance explains that the lessor must take into account the amount of compensation as income received when determining the object of taxation. And payment for telephone services is included in expenses.

Despite the fact that the letter was sent to landlords who are on a simplified taxation system, the conclusions of the Russian Ministry of Finance are based on the articles of Chapter 25 of the Tax Code “Organizational Income Tax.” Namely, Article 249, which affects the concept of income, and Article 259, which regulates expenses.

Therefore, a taxpayer under the general taxation regime must take it into account.

The author is the head of the Department of Methodology and Consulting of CJSC “Business Profile”, full member of the Chamber of Tax Consultants of Russia, IPB of Russia and IPB of the Moscow region

HAVE TIME BEFORE NG!

The most visited Clerk course on management accounting is already taken by more than 100 of your colleagues. Hurry up to sign up for the course at the old 2021 price. Then it’s more expensive. Pay now, study in 2022 in a convenient stream.

- Duration 120 hours in 1 month

- Your ID in the Rosobrnadzor register (FIS FRDO)

- We issue a certificate of advanced training

- The course complies with the professional standard “Accountant”

View full program

How and where to check?

Initially, it is worth checking the availability of these funds in the bank account whose coordinates were transferred to social security. You can do this at the bank itself, or via the Internet if a card is linked to your account.

If there is no money, and all the deadlines have already passed, you need to contact the social security service itself to find out whether they transferred the funds to you at all, and if not, then why.

Who pays?

The subsidy is awarded by social security authorities at the place of registration of the person who requested this assistance from the state. Funds for subsidies and other assistance to the population are provided from the budget.

Where is it paid?

The subsidy for housing and communal services comes to a bank account or card, and most social security authorities work with Sberbank, since it is state-owned . You can clarify this issue with your local social security office, as there may be different options depending on the region. In most cases, we are talking about Sberbank, where you need to get a book or card and open an account. It will receive state aid funds, which you can subsequently withdraw at any time.

Innovations in 2021

Utility prices have changed since 2021. The increase occurred in January and June. In January, tariffs increased by 1.7%, and in June - by 2.4%. This happened due to an increase in the amount of VAT established by the state. Tariffs will continue to rise in 2021.

The two-stage increase in rent tariffs serves to synchronize tax and tariff legislation. Also, changes in the amount prevent tariffs from rising above the projected inflation target.

Types of assistance from the state

For vulnerable categories of citizens, there are 2 types of support from the state:

- Privileges. This type of support is intended to alleviate the financial situation of a special category of citizens—beneficiaries. The government provides support, including by reducing rent. Relaxations are established at the federal level, but sometimes at the expense of regional budgets. Discounts on utilities are issued only for one housing where the recipient is registered and lives.

- Subsidies. This type of assistance is also intended for beneficiaries, but not in the form of a reduction in fees. Subsidies imply cash payments or compensation for payments from the state. They are assigned to those families whose earnings are below the established minimum, and at least 22% of the total family income is spent on payments for living space. The percentage indicator is averaged; different minimums are set for different areas. In some cities, it is enough to spend 10% of your income to qualify for government assistance. But some beneficiaries receive a portion of their expenses back even if their expenses do not reach the established limit. These include liquidators of the Chernobyl Nuclear Power Plant, disabled people, and WWII veterans.

In Russia and Ukraine, citizens who are not included in the register of beneficiaries are not assigned either benefits or subsidies. But in Ukraine, the state provides a choice to preferential categories: they can receive either discounts on rent or compensation for part of the money spent.

Refund of part of the amounts paid

The application and the rest of the documentation for the refund are submitted to the MFC or the social protection department of citizens. Basic list:

- photocopies of passports of all family members;

- document on family composition;

- certificate of ownership of real estate;

- documents that confirm relationship for each family member;

- certificate from the BTI;

- six-month receipts for utility payments to check the absence of debts;

- documents for each family member about his personal income;

- a photocopy of the work record book, an extract from the savings book;

- certificate from the employment center, only for the unemployed.

You can submit documents during a personal visit to the MFC or social protection department or online through the State Services portal. The application processing period takes a maximum of 10 days.

When calculating the amount of compensation, the total income of all family members is taken into account. But for each individual tenant you will need a 2-NDFL certificate. The compensated amount can be sent directly to the company’s account and taken into account in future payments. Or the money can be sent to the utility account of the beneficiary.

You will need to re-register compensation twice a year. Moreover, it is recommended to do this until the middle of the month. When sending an application in the first 2 weeks of the month, subsidies are accrued in the current month. And if you submit documentation in the second half of the month, benefits begin only in the next month.

If, while receiving subsidies, the beneficiary has debts or delays of 2 months or more, then the right to compensation disappears. Utilities are suspending compensation. To receive funds again, you will need to pay off the debt and apply for subsidies again.

5 / 5 ( 1 voice )

about the author

Klavdiya Treskova - higher education with qualification “Economist”, with specializations “Economics and Management” and “Computer Technologies” at PSU. She worked in a bank in positions from operator to acting. Head of the Department for servicing private and corporate clients. Every year she successfully passed certifications, education and training in banking services. Total work experience in the bank is more than 15 years. [email protected]

Is this article useful? Not really

Help us find out how much this article helped you. If something is missing or the information is not accurate, please report it below in the comments or write to us by email

Example of calculating benefits for a disabled person

To calculate housing and communal services benefits for a disabled person, let’s take the example of a family of 4 people. They live in Moscow, where 1 kV of electricity costs 5.8 rubles. One of the family members living in the apartment is disabled.

For 1 month, the family consumed 160 kW of electricity. The portion spent by the disabled person: 160 / 4 = 40 kV of electricity. 40 * 5.8 = 232 rubles - this is the discount amount provided for a disabled person. If there are two beneficiaries in a family, then calculations of housing and communal services benefits are made taking into account two people: 160/2 = 80, the amount of the benefit will be 464 rubles. In this way, you can calculate the total amount of savings for each utility service separately.

Regional benefits and subsidies

The regional government has the right to establish rent benefits in its administrative district. For example, in St. Petersburg, the local government returns half the amount spent on housing and communal services:

- home front workers during the Second World War;

- veterans of labor and war;

- pensioners whose work experience is 45 years for men and 40 years for women;

- rehabilitated after repression;

- women who gave birth and raised 10 or more children;

- Large families with up to 10 children receive a 30% discount on rent.

The government of Nizhny Novgorod compensates expenses for utilities only for labor veterans whose monthly income does not reach 21,673 rubles.

Reduced payments and refunds apply only to a certain area of housing. Quadrature restrictions:

| Number of residents | Limit |

| 1 person | 33 sq. m |

| 2 people | 42 sq. m |

| 3 occupants or more | 18 sq. m for each |

If the housing area exceeds the established limits, the extra square meters. meters the state does not subsidize or pay for. That is, the beneficiary is obliged to pay the excess square footage at a 100% tariff.